It’s the first day that America’s small businesses can apply for the SBA’s Paycheck Protection Program, i.e., the $350BN program that is part of the bigger $2 trillion bailout package designed to provide small businesses access to capital for payroll and other overhead costs to the tune of 2.5 months of average payroll and which must be accessed via an existing banking relationship – and the rollout is predictably a mess, with some banks such as BofA already accepting loans (which convert to grants if used exclusively for payrolls and business continuity purposes), while others like JPM delaying the roll out to 1pm; a third group of banks such as Wells Fargo has conspicuously failed to provide its rollout plans – perhaps it is scheming how to cross-sell bailout loans with auto insurance or engage in some other typically Wellsfargoian fraud.

$WFC will not be ready to take applications for #PaycheckProtectionPlan today. They’re doing all the can and testing constantly. When you and running you will have to have a checking account and be an online banking customer to qualify. No previous loan requirement.

— Wilfred Frost (@WilfredFrost) April 3, 2020

But a recurring shock as millions of small business owners head to these bank websites to apply for the PPP funds is that contrary to the SBA’s guidance that any small business with 500 or less employees can apply, going to lender portals shows that only a very narrow subset of America’s millions in small businesses are be eligible.

In fact, only those companies that already have a lending relationship, i.e., an outstanding loan with a given bank are – at least as of this moment – able to apply for the rescue funds.

Moynihan making clear on @SquawkStreet that small businesses should not only apply to their existing bank – but primarily to their existing LENDER. Just having a small business checking account will not suffice initially – you need to have borrowed from $BAC in recent past. https://t.co/LvSqMg3Rf8

— Wilfred Frost (@WilfredFrost) April 3, 2020

Bank of America’s website confirms as much, stating on its eligibility page that only “clients with a business lending and a business deposit relationship at Bank of America are eligible to apply for a Paycheck Protection Program through our bank.” In other words, any business that only has a deposit account and no loan or business card is out of luck.

And the kicker, literally, for those BofA clients who would like to become eligible and open a business loan account, well it’s too late: as the bank makes clear, this should have happened as of Feb 15.

To apply for the Paycheck Protection Program through our bank, you must have a pre-existing business lending and business deposit relationship with Bank of America, as of February 15, 2020. A Business Credit Card, line of credit or loan may be the lending product used.

Said otherwise, business who ran a clean balance sheet without debt are seen as riskier than businesses that carry loans, and are unduly penalized just because they never opened a loan with BofA.

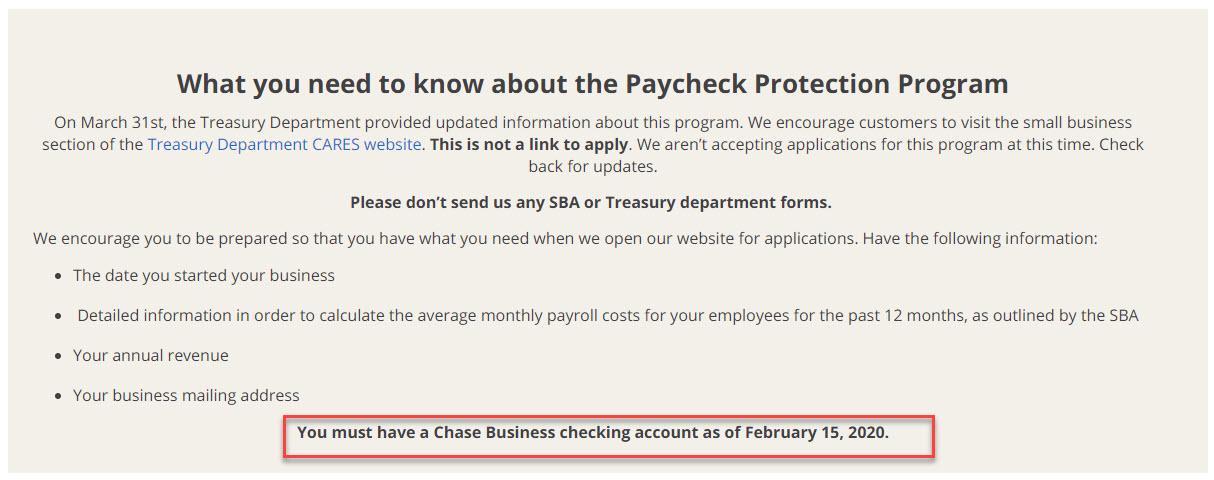

JPMorgan is even more draconian in its selectivity of whom it will hand out Treasury-guaranteed money to. As the bank notes in its ironically-named “CARES” website, “You must have a Chase Business checking account as of February 15, 2020.” Anyone who does not is straight out of luck.

And as countless other banks follow suit, the question becomes is this how the banks that were bailed out by ordinary Americans in 2008 will treat those same Americans when they need a rescue too? Alternatively, what happens to these banks when millions of small business fail and America’s economy plunges into an even deeper depression. One final question: how is it logical for banks to only bailout those companies which already have debt and are by extension riskier, than to provide funds to their ordinary clients who only now, for the first time, need a helping hand.

We eagerly await Steven Mnuchin’s answers to these questions.